Are Your Small Business Benefits Risking Your Employees' Marketplace Subsidies?

If you are a small business owner thinking about offering benefits or expanding your current benefits package, you may worry about preventing employees from being eligible for subsidies if they decide to purchase Marketplace coverage.

In This Article

In our work designing benefits packages for small businesses, one common topic we often find ourselves clarifying for clients is the impact of the Affordable Care Act (ACA) on health insurance accessibility and affordability, especially when it comes to employer-sponsored benefits. At Planstin, our goal is to make benefits accessible to more people. As part of this, we want to address and resolve confusion and help employers offer benefits with confidence.

The ACA, the Marketplace, and subsidies

One of the ways the ACA expands access to health insurance for more Americans is through the Health Insurance Marketplace, a platform where users can compare and purchase health insurance coverage. While the health insurance available on the Marketplace does have standard market premium costs, the ACA allows for subsidies for those in lower income brackets. These subsidies, essentially financial assistance from the government, make coverage purchased through the Marketplace more affordable.

Another mechanism through which the ACA expands access to health insurance is by imposing requirements and considerations on businesses based on their size.

Businesses with More Than 50 Full-Time Employees

These businesses are considered large employers under the ACA and are required to provide health insurance that meets the ACA’s standards of Minimum Essential Coverage (MEC), Minimum Value, and

affordability. If a business of this size fails to comply, either by offering no health coverage or insufficient health coverage, this results in financial penalties. These penalties help incentivize large businesses to offer these types of benefits.

The ACA allows subsidies for those in lower income brackets. These subsidies, essentially financial assistance from the government, make coverage purchased through the Marketplace more affordable.

- Minimum Essential Coverage: This is the type of coverage an individual needs to have to meet the ACA’s individual responsibility requirement (often termed the individual mandate). Most employer-sponsored health benefits meet this standard.

- Minimum Value: The ACA considers a plan as meeting Minimum Value standards if it covers at least 60% of the total cost of medical services for a standard population, as well as substantially covers inpatient hospitalization services and physician services.

- Affordability: For 2024, the affordability threshold is set at 8.39% of an employee’s household income. If an employer only offers insurance that costs an employee more than this, it is considered unaffordable under the ACA.

Businesses with Fewer than 50 Full-Time Employees

Small businesses fall outside the mandate that requires providing health insurance, and thus the requirements listed above do not apply to them. However, many small businesses still choose to offer health benefits to attract and retain talent on their teams. The ACA provides options and incentives for small businesses in these scenarios, including the Small Business Health Options Program (SHOP) Marketplace, to help make purchasing health insurance more manageable for small employers.

As mentioned earlier, subsidies play an important role in expanding health insurance access, but these subsidies aren’t available to everyone. Only those with low-to-mid-level incomes that do not have ACA-compliant employer-sponsored benefits options available to them can qualify for these subsidies.

What ends up confusing some employers is whether offering any health benefits will make it so their employees can’t access these subsidies. To clarify: you can offer your employees health benefits without jeopardizing their eligibility for marketplace subsidies. Let’s see how.

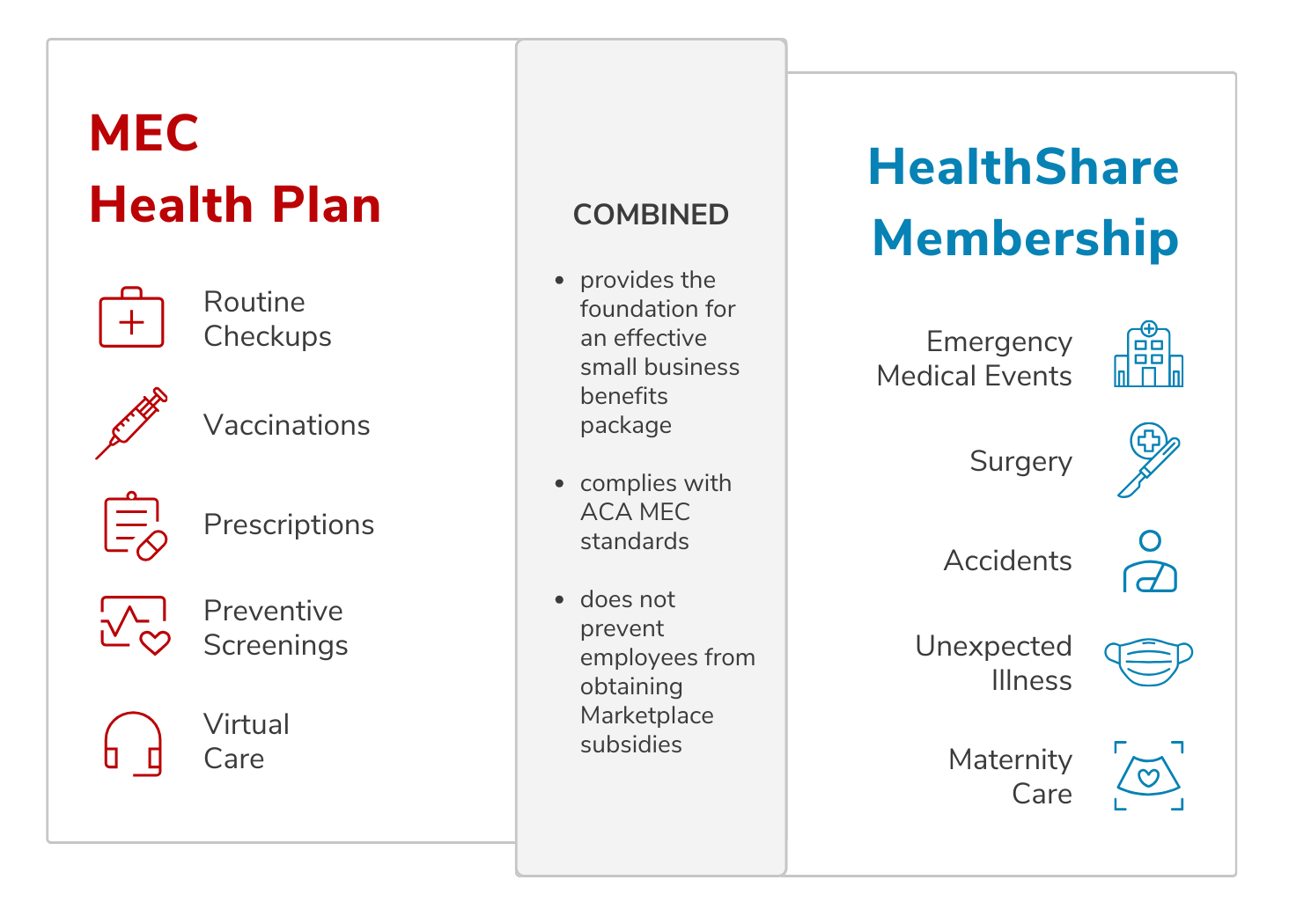

MEC + HealthShare: An affordable alternative

Preventive MEC plan designs focus on preventive care services. They are specifically designed to cover basic health services, including preventive care like routine checkups, immunizations, and screenings that can be important for maintaining health and preventing illness. As MEC-compliant plans, they allow employees to meet the individual mandate, but they do not include the more comprehensive benefits of a Minimum Value-compliant health plan.

To complement the preventive care provided by a MEC plan and fill the gaps for larger unexpected medical needs, Planstin partners with Zion HealthShare to provide clients access to HealthShare membership options. HealthShares are not insurance, but instead are a cooperative medical cost sharing program through which funds are pooled by members and distributed to those with eligible medical costs.

MEC vs MV: What’s the Difference?

Because the ACA imposes a mandate for individuals to have insurance, the MEC standard must be met to satisfy this individual mandate. Simply put, the distinction between the two is that MEC is about coverage requirement, and MV is about coverage quality.

It should also be noted that while previously individuals might face penalties for not meeting the individual mandate, these penalties are not currently in effect.

This model supports members in managing larger and unexpected medical expenses, particularly for events or treatments not covered under a preventive MEC plan. You can learn more about Zion HealthShare membership here.

For small businesses seeking to offer more well-rounded health benefits while managing costs, combining MEC with HealthShare membership offers a balanced and affordable solution. This combination provides employees with access to essential preventive services while also providing a safety net for more significant medical expenses through a supportive community-based approach.

What MEC + HealthShare won’t do, however, is disqualify your employees from Marketplace subsidies.

As a small business owner, you may want to offer affordable benefits like MEC + ZHS but are concerned that having this option available might make your employees lose out on subsidies they could use to buy coverage through the Marketplace. In reality, this should not be a concern, and you can rest assured that Planstin will help you design a plan to support your employees’ health without affecting their eligibility for subsidies.

Offering MEC + HealthShare does not impact subsidy eligibility

The simple answer here is that MEC plans do not meet the ACA’s Minimum Value standards for comprehensive health coverage. And because HealthShare membership is not a form of insurance, it also does not meet the Minimum Value criteria. With this being the case, your employees can still qualify for subsidies if they choose to purchase insurance through the marketplace.

You can offer your employees health benefits without jeopardizing their eligibility for marketplace subsidies.

When subsidy eligibility may be affected

Typically, employees’ eligibility for Marketplace subsidies are affected at larger companies where the ACA’s requirements apply. If a company opts to provide plans that meet these standards, such as a Care+ plan, employees’ subsidy eligibility could be affected, even if they choose not to enroll.

But when businesses with fewer than 50 employees, who are not subject to the employer mandate, choose to offer a MEC + Zion HealthShare combination, the scenario is different. Their employees are not disqualified from Marketplace subsidies if they offer MEC + HealthShare.

Tailor your benefits

At Planstin, we help you design a benefits package to do the most good for your company and employees. Our approach is tailored, recognizing that while we do work with plan designs that meet the ACA’s Minimum Value requirements, these plans are not necessarily the answer for small businesses that are not required to offer them. This understanding shapes our ability to help clients with MEC + HealthShare combinations— packages designed to offer a well-rounded healthcare solution without risking your employees’ eligibility for Marketplace subsidies.

If you’re a small business owner looking for benefits designed to fit your needs, there are solutions for you.

SUGGESTED FOR YOU