How to Talk to Your Employees About Nontraditional Benefits

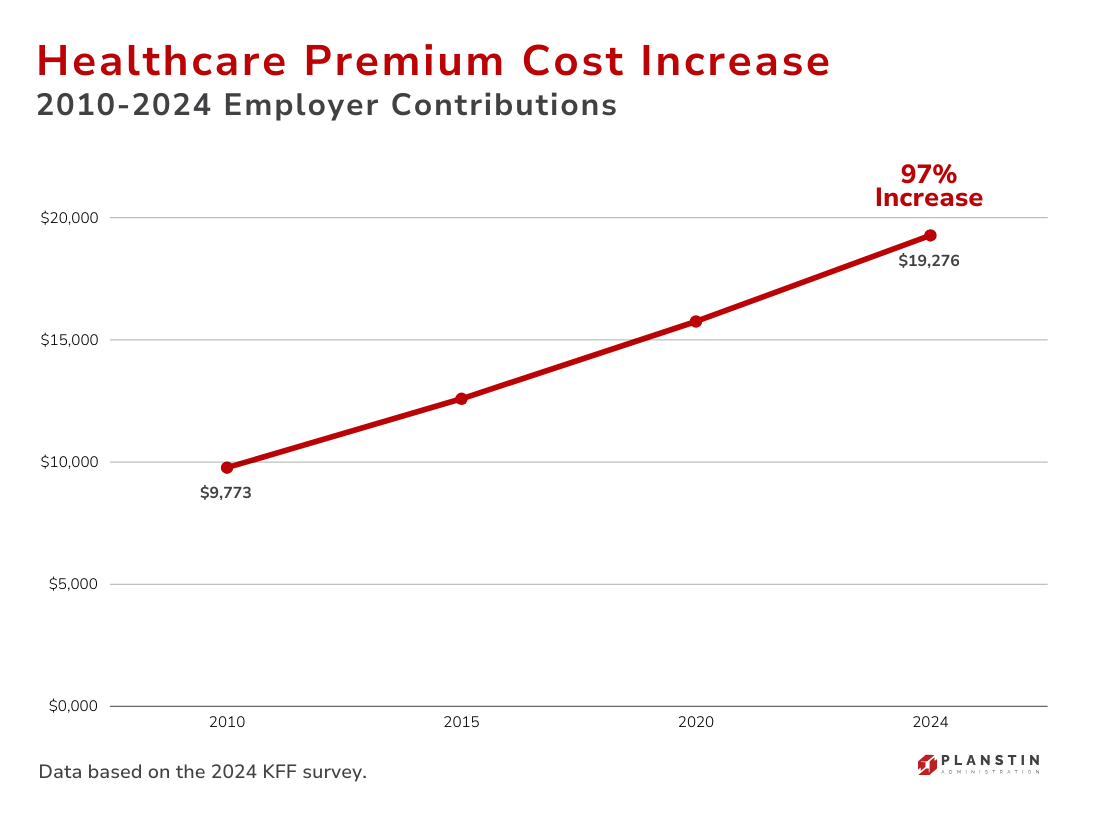

For many business owners, the rising costs of traditional health insurance have created a challenging dilemma: how to provide valuable benefits without straining company finances. However, the recent rise of nontraditional healthcare options has made it easier for employers to provide fair benefits to their employees, without breaking the bank. What might not be as easy is introducing them to your team.

In This Article

Nontraditional healthcare solutions are gaining popularity because they offer a refreshing change: flexible, affordable options that benefit both employers and employees. If you are considering nontraditional benefits, it’s important to think about how these options will impact your team and to communicate those benefits effectively.

Educating employees on how these insurance alternatives work and what they offer can help them make the best decisions for their health and well-being.

What are health insurance alternatives?

Health insurance alternatives are options that offer medical care outside the traditional insurance model. While they may not cover every possible medical need, they can be a great fit for people who are looking for a cost-effective way to manage their healthcare.

There are several types of health insurance alternatives including direct primary care (DPC), health savings accounts (HSAs), short-term insurance, association health plans, health discount cards, medical cost sharing programs, and virtual care. In this guide, we’ll take a closer look at three increasingly popular options—direct primary care memberships, HealthShare programs, and virtual care—and explore how you can introduce and begin to explain these choices to your employees.

Direct primary care (DPC)

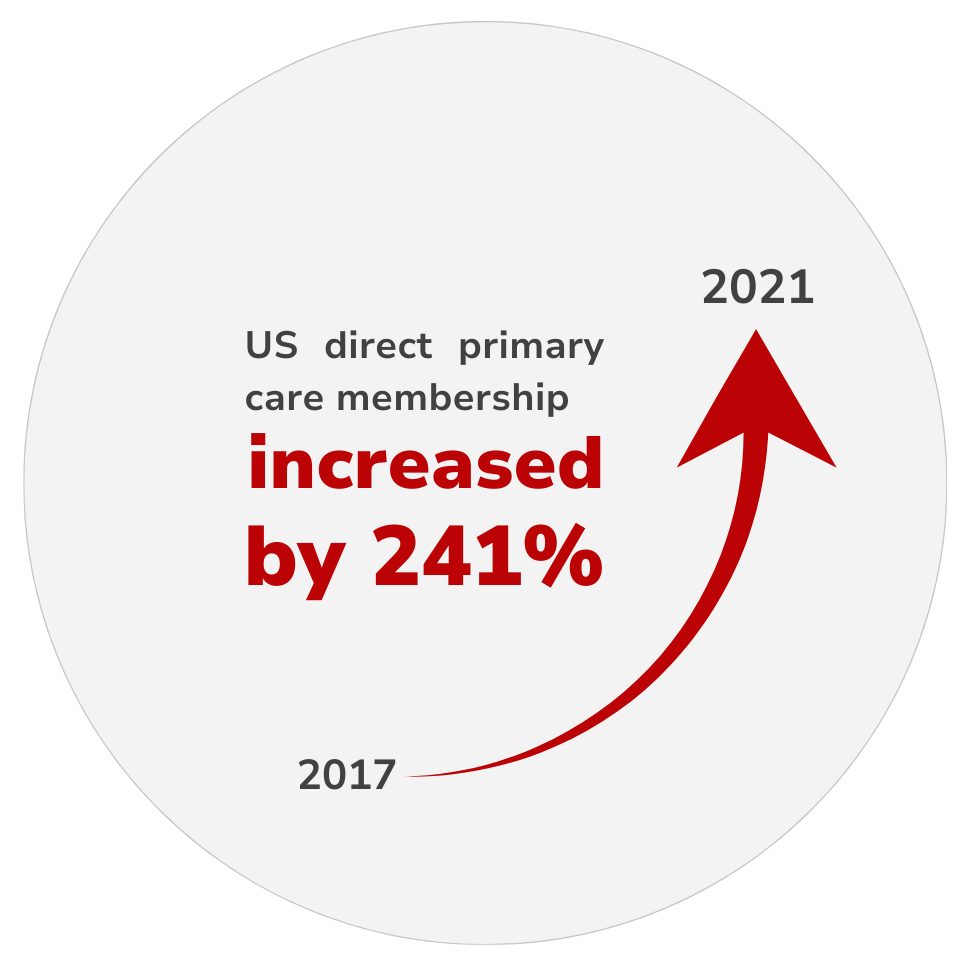

In a world where subscription services make everything from entertainment to meal planning easier, it's no surprise that DPCs are becoming a popular choice for healthcare. In fact, direct primary care clinics have seen a 241% increase in membership across the U.S from 2017 to 2021.

Direct primary care clinics operate on a straightforward subscription model: patients pay a monthly membership fee for direct access to their medical provider and the services included in their membership. Because DPCs don’t accept insurance, they’re often referred to as “cash-only” practices. By removing the insurance middleman, DPCs can keep costs low while focusing on quality and personalized care.

Each DPC clinic can vary in focus. Some specialize in areas like sports medicine or wellness, while others provide family medicine and general preventive care. A typical family medicine DPC covers services like annual exams, routine screenings, and lab work within the monthly membership. Additionally, DPC memberships generally provide unlimited access—and often times remote access—to their care provider. However, it’s important to communicate that specialist visits, urgent care, hospital stays, and prescriptions are typically not included in a DPC membership.

What it Does

- Preventive and routine care: Convenient access to general healthcare needs and routine checkups.

- Affordable pricing: Low monthly fees and no deductible makes virtual care accessible to more people.

- Direct access to care: Connect with providers easily, without navigating insurance requirements.

- Transparent costs: Clear pricing with no hidden fees or surprise out-of-pocket expenses.

What it Doesn’t Do

- Emergency care: Not intended for urgent or emergency medical situations.

- Specialty care: Limited in scope for specialized treatments or in-depth medical procedures.

Why Should Employers Consider Offering a DPC?

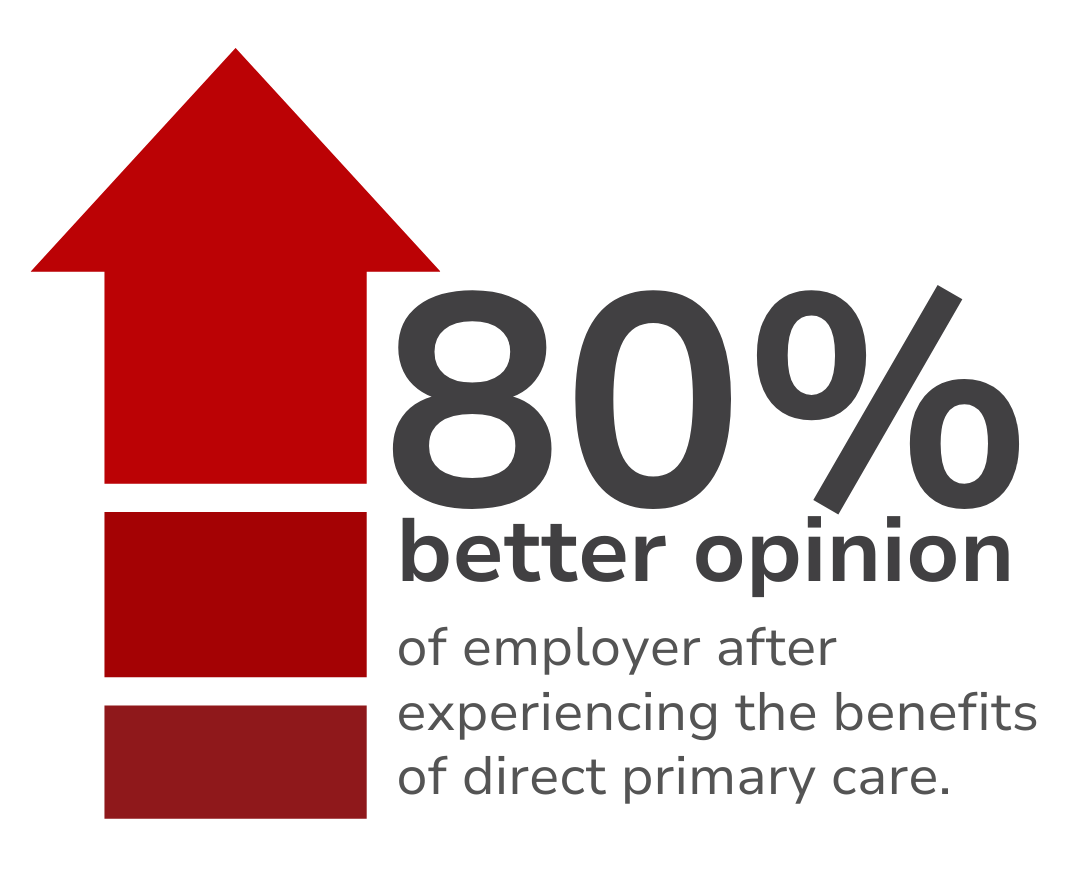

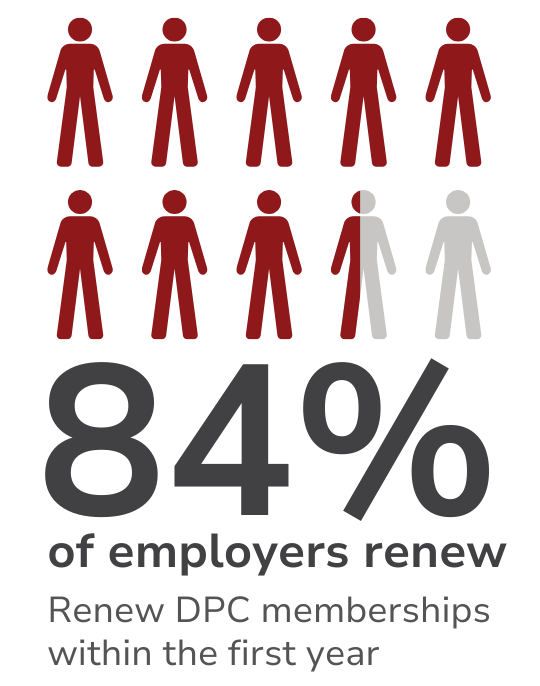

Employers are increasingly drawn to direct primary care for its potential to improve employee well-being and satisfaction. According to Hint Health’s 2022 DPC Consumer Insights Survey, 84% of employers who offer a DPC renew it within the first year. In fact, a 2019 study on large group cases found that employees’ opinions of their employers improved by 80% after experiencing the benefits of their DPC.

One of the greatest advantages of DPCs is their focus on building a personal connection between patients and their primary care provider. Having a doctor who is readily available and familiar with an individual’s health history can lead to better health outcomes and a stronger sense of care. For both employers and employees, DPC membership often means lower costs and more accessible, stress-free healthcare—a win-win that promotes satisfaction and health across the board.

3 Key Points to Communicate to Employees

When introducing DPCs to your team, avoid making recommendations for specific employees; rather, provide clear and concise general information. Here’s what to you may want to emphasize:

- Subscription model: Explain that DPCs operate on a simple monthly subscription.

- Focus on preventive care: DPCs generally cover routine and preventive care but do not handle emergencies or specialized care.

- Complementary pairing: DPCs can be paired with other benefits, like a HealthShare.

HealthShare

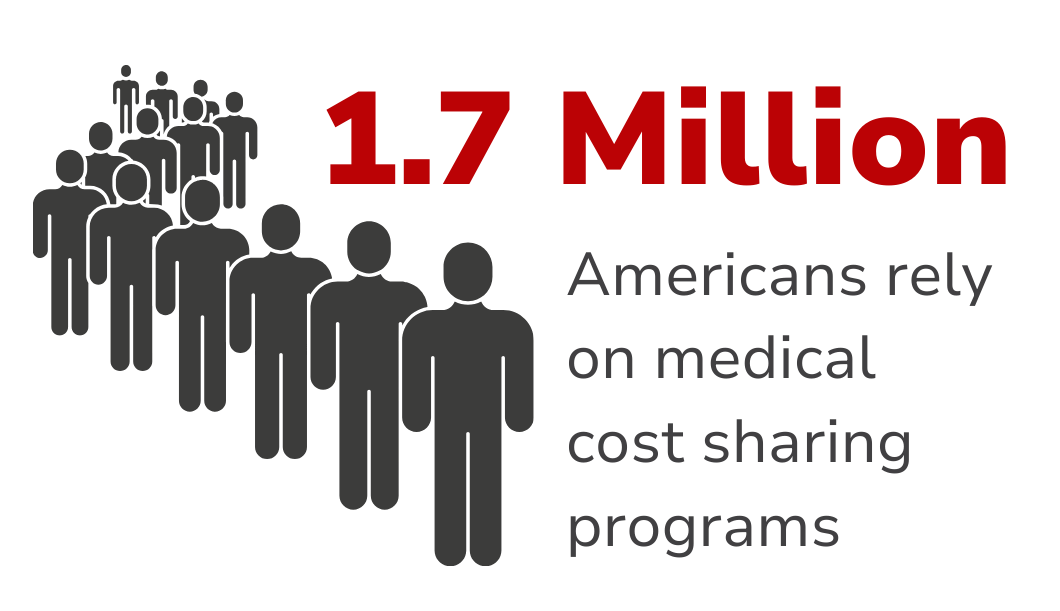

HealthShares might be a new concept for you and your employees. However, they are quickly growing in popularity, as more than 1.7 million Americans rely on medical cost sharing plans.

Health sharing is a health insurance alternative that provides a safeguard against large medical bills through a community-driven approach. Rather than being insured through a company, members contribute to a community fund that is used to help share eligible medical bills. Here’s how it works: members pay a monthly membership fee, and when a medical need arises, they visit a provider as a self-pay patient, covering an initial portion of the costs themselves (similar to a deductible). After that, the HealthShare steps in to help share qualifying expenses from the community funds.

Monthly membership fees are flexible and can often be tailored to fit individual needs. Typically, a higher monthly fee means a lower initial amount toward medical expenses, while a lower monthly fee means a higher initial out-of-pocket amount. This flexibility can make HealthShares especially attractive for individuals or families seeking an affordable safeguard against costly emergencies.

HealthShares are designed to be a financial protection for unexpected events, like ER visits, and other big medical bills, such as those for surgery or maternity. Each HealthShare has specific guidelines for what is and isn’t shareable, with a primary focus on significant medical expenses rather than routine care.

What it Does

- Affordability: HealthShares operate on a cost-sharing basis, often providing more budget-friendly options than traditional insurance.

- Flexibility: Members aren’t tied to specific networks, allowing them to choose their providers freely.

- Transparency: Membership fees are generally clear-cut and list the medical events that are and are not shareable in the member guidelines.

- Anytime enrollment: Members are not under any kind of contract, meaning employees can sign up whenever it’s convenient for them.

What it Doesn't Do

- Not insurance: HealthShares aren’t insurance and operate differently.

- Not MEC: Since they don’t need to follow ACA regulations, they do not qualify as Minimum Essential Coverage (MEC), and members should not expect a HealthShare to “cover” everything a typical health plan might.

- Selective sharing: HealthShares only share expenses for qualifying events that align with their guidelines, which means not all types of medical events are included. Additionally, certain needs may only be shareable after a waiting period.

- Risk of out-of-pocket costs: Because sharing is limited to eligible events, members will pay for unshareable expenses.

Why Should Employers Consider Offering HealthShares?

Employers are exploring HealthShares as a cost-effective alternative to traditional health insurance. HealthShares give employees the peace of mind that they’re protected in case of emergencies. The option to choose different membership tiers allows employees to find a plan that fits their unique needs. HealthShares also lighten the administrative load with less paperwork and fewer complexities, making things easier for HR teams. And with year-round enrollment, new employees can be onboarded quickly—keeping healthcare accessible from day one. This flexibility empowers employees and employers to prioritize their financial and healthcare needs in a way that works best for them.

3 Key Points to Communicate to Employees

Since HealthShares might be unfamiliar to some employees, it’s essential to introduce the concept with patience and clarity. If you are working with a broker or benefits administrator, it may be best to have them educate your employees about the finer details. When introducing this as an option, you might highlight these points:

- Not insurance: HealthShares are cost-sharing memberships rather than traditional insurance.

- Coverage limits: While HealthShares can be affordable and supportive during emergencies, they don’t share in all medical expenses. Make sure your employees have access to the member guidelines.

- Pairing with other options: HealthShares can be paired with alternatives like MEC plans or DPC memberships to fill gaps, especially for routine care needs.

Virtual care

According to Wheel's (who surveyed more than 2,000 consumers) 2023 Consumerization of Care Survey, the demand for virtual healthcare options is rising quickly. Their report showed that around “64% of consumers would prefer to see their primary care provider virtually” if given the choice.

Virtual care makes healthcare more accessible by using technology to provide a range of digital health services beyond traditional, in-person visits. It encompasses everything from telemedicine (remote clinical appointments) to wellness coaching, mental health support, general medicine, and even patient advocacy. Some virtual care clinics offer broad services, while others specialize in areas like primary care or mental health support. Many direct primary care (DPC) clinics also incorporate virtual care, allowing patients to connect with their doctor remotely as needed.

Payment models for virtual care vary based on the provider and your specific needs. Some services operate on a pay-per-visit basis, while others offer subscription plans. Whether through video chats, texts, or phone calls, virtual care uses flexible technology to work with you on your schedule. While some appointments may require scheduling, virtual care often provides 24/7 access, offering quick and convenient support when you need it most.

What it Does

- Convenient access: Ideal for those in rural areas, busy professionals, or individuals who may have difficulty visiting a doctor in person, like elderly patients.

- Time-saving: Patients can access care without taking time off work or traveling to a clinic, reducing the impact on their day.

- Cost-effective: Virtual care often comes with a low monthly fee and no deductible, making it an affordable option.

- 24/7 support: Provides round-the-clock access to healthcare professionals, so help is always available, whether it’s a common illness or general health question.

- Quick diagnoses for minor issues: Simple ailments, like a sore throat or cold, can be diagnosed remotely, helping prevent the spread of infectious diseases by avoiding waiting rooms.

- Guidance for non-emergent concerns: Patients can receive advice for non-urgent issues before resorting to costly ER visits, ensuring they get the right care when needed.

What it Doesn’t Do

- Emergency care: Virtual care is best suited for non-emergency issues and is not a substitute for urgent medical care.

- Continuity of care: For patients seeing different providers virtually, it can be challenging to build a rapport with their provider.

- Technology requirements: Patients need reliable internet access and a smartphone or computer to use virtual care services.

- In-person care for certain appointments: Some healthcare needs, like specific exams or procedures, still require an in-person visit.

Why Should Employers Consider Offering Virtual Care?

Virtual care is a convenient, cost-effective healthcare option that meets the needs of today’s busy workforce. By offering virtual care, employers can help employees access healthcare easily, saving them time and reducing the need to take paid time off for appointments. Virtual care also removes the logistical challenges of visiting a doctor in person, which is especially valuable for employees in remote areas, those with mobility limitations, or anyone balancing a demanding schedule.

For employers, virtual care simplifies benefits management with fewer administrative tasks and often lower costs. Plus, with 24/7 access to healthcare professionals, employees are more likely to seek care when they need it, promoting overall well-being and helping prevent minor issues from becoming major ones. Offering virtual care supports a healthier, more engaged workforce and demonstrates a commitment to flexible, accessible healthcare that benefits everyone involved.

3 Key Points to Communicate to Employees

When explaining virtual care to employees, remember to cover these key points:

- Explain access: Provide clear instructions on how to access virtual care services.

- Outline what’s included: Share a summary of the specific services that your virtual care provider does and does not offer.

- Pairing with other benefits: Help employees see how virtual care can work alongside other healthcare options, like DPCs, to offer a comprehensive care plan.

Best practices for communicating nontraditional healthcare options to employees

Nontraditional healthcare options may be new to many. So, clear, open communication is essential to help your employees make the best choice for their needs. Here are some ways to approach the conversation and create a positive experience for everyone involved:

Be Transparent

Each option has its own pros and cons that vary depending on individual needs. Simply present the facts and let employees decide what works best for them.

Clarify the Differences

Explain that healthcare alternatives aren’t insurance. Discuss what these options cover and what they don’t, referring back to the “what it does” and what it doesn’t do” sections in this article as needed.

Be Prepared for Questions

Anticipate common questions and have straightforward answers ready to go. This builds trust and helps employees feel supported.

Use Simple Language

Avoid industry jargon or technical terms. Instead, opt for clear, everyday language that everyone can understand.

Provide Multiple Ways to Reach Out

Schedule an informational meeting, send follow-up emails, and make it easy for employees to get answers to their questions.

Lean on Your Administrator for Guidance

Your benefits administrator is a key resource in understanding your healthcare options. Reach out to them for support in making these options clear and accessible for your team.

Exploring nontraditional healthcare options

There are times when traditional insurance is the best choice, especially for employees with chronic medical needs. However, many covered services in traditional insurance plans go unused, leaving both employers and employees paying for benefits they may not use to the full extent. Nontraditional healthcare options offer a flexible, cost-effective way to support your employees' health, often at a fraction of the cost.

While nontraditional benefits might be a new concept for some, they don’t have to be intimidating.

By exploring these insurance alternatives and communicating their advantages and limitations with clarity, you can help employees understand their options and feel more comfortable choosing the best fit. The more you educate and support your team through this process, the more likely they are to feel confident and satisfied with the benefits you offer.

Want to explore insurance alternatives for your business? Chat with one of our Benefit Guides about how insurance alternatives can add value to your benefits offering.

Explore

SUGGESTED FOR YOU