Why Are Businesses Looking for Alternatives to Insurance?

Businesses are being let down by the insurance industry—and their employees are already paying the price. With healthcare premiums likely to increase by 9% in 2025, many employers are being backed into a corner. Forced to decide between their budget and their people, businesses are looking for a Hail Mary.

In This Article

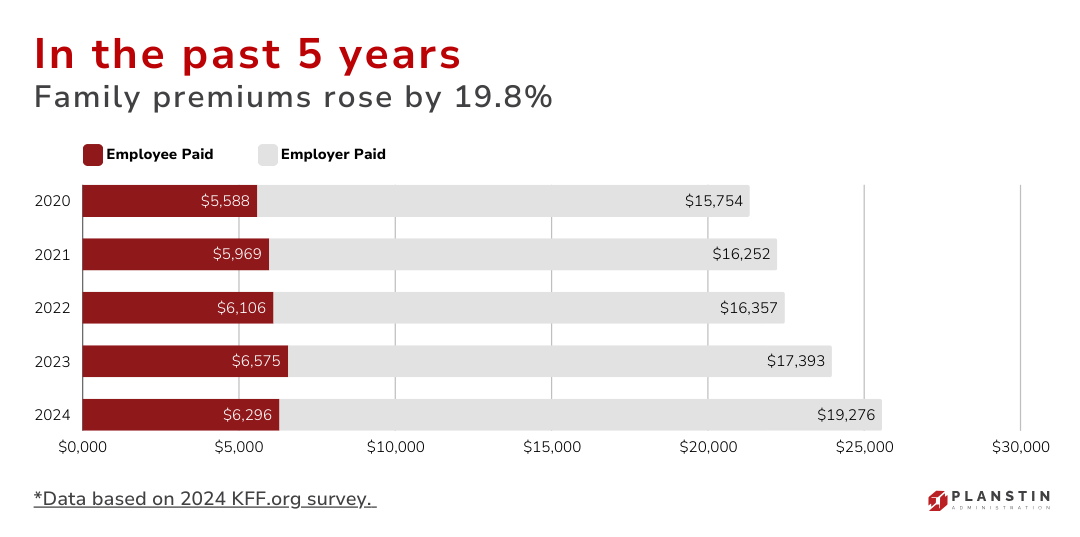

While employees are certainly not immune from healthcare’s economic pressure —family premiums have skyrocketed over the past five years, and annual pay increases can’t keep up—employers are feeling the financial squeeze exponentially more acutely.

Employers typically cover 81% of health plan costs. And when premiums increase, as they inevitably do, employers absorb the majority of the blow.

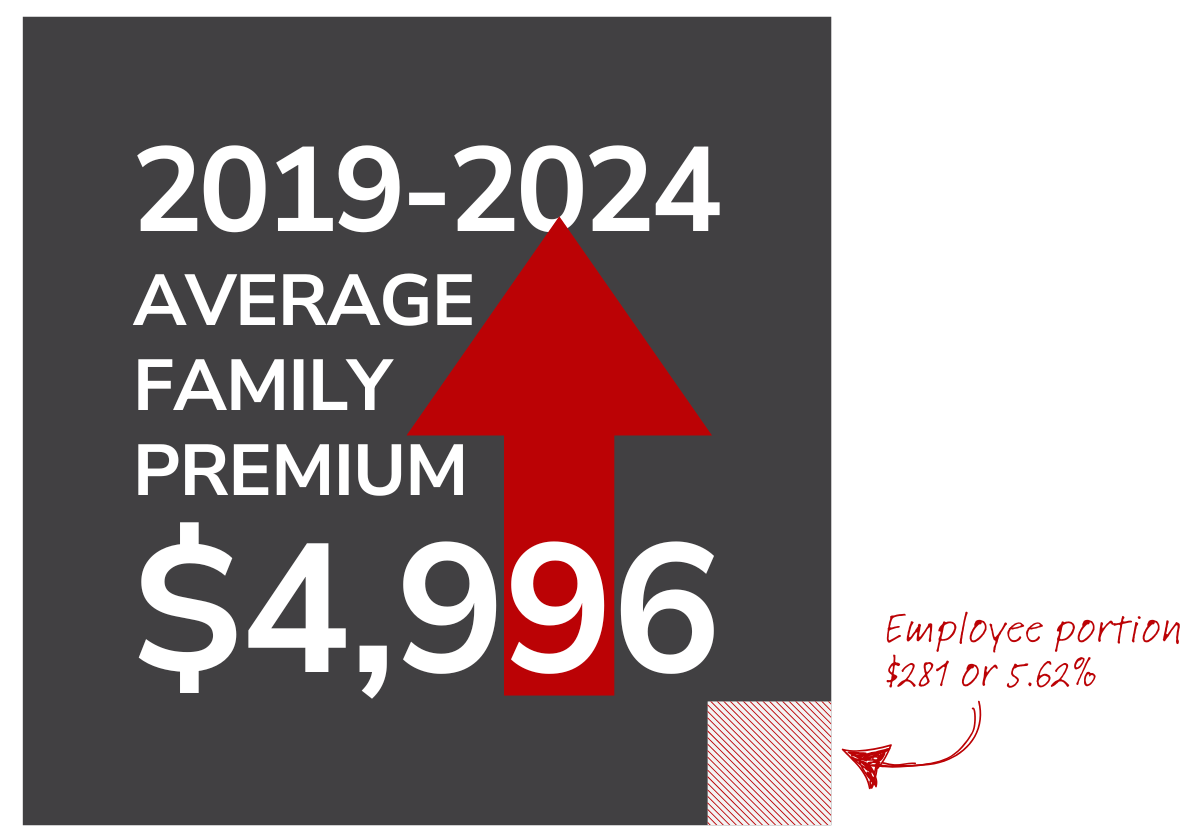

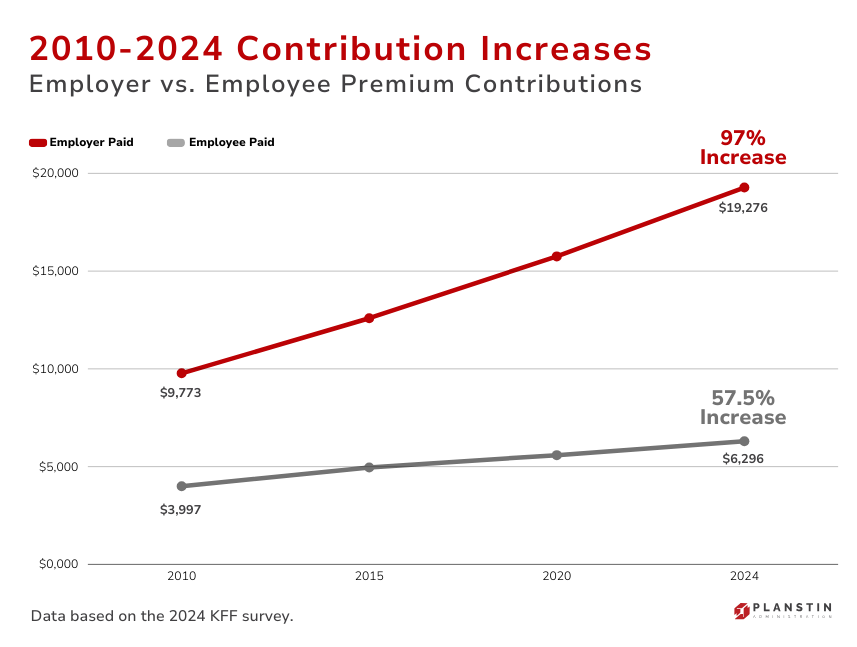

To highlight the impact of this on employers, in the past 5 years family premiums have risen by 24%, or just under $5,000; employees are paying less than $300 of that.

In fact, on average, employers are paying a whopping 94.38% of that family premium increase (employees paying for 5.62% of the overall increase).

Cost challenges for large employers

In particular, the costs are piling up for larger employers offering traditional coverage. The ACA employer mandate requires employers to keep healthcare costs within certain affordability parameters, which generally means keeping the employee’s portion to around 9% of their annual household income.*

Premium increases have averaged about 4.4% since 2019, and every year employers have to contend with higher and higher costs at renewal. Unfortunately, 2025, is looking to exceed this average with the highest annual increase in years. Depending on who you ask, forecasters are predicting increases between 6%, and 9%**, but some of our new clients who have found us while shopping for other options have cited numbers closer to 15%.

Why are costs rising so dramatically? Employers surveyed by the International Foundation on Employee Benefit Plans cite specialty drugs, catastrophic claims, and provider costs as the top three reasons. These responses demonstrate the unpredictable nature of medical claims and the difficulty that presents for employers looking to manage costs.

Administrative difficulties for small and mid-size businesses

For small and mid-size businesses, the situation is not much better. Although they are not held to the same federal standards as larger companies, small businesses have their own gauntlet to contend with. For starters, the administrative challenges of offering benefits—coordinating enrollments, dealing with claims, managing regulatory concerns—can overwhelm even dedicated HR teams, much less a one-person department or business owner trying to do it all.

On top of the administrative burden, competing for employees against larger, more competitive companies can be daunting. Looking at what large companies are able to offer can be discouraging for small and mid-size businesses who feel like they simply can’t compete. For these businesses, adding on the pressure of relentless high-ticket premium increases presents such a financial strain that they either are in desperate search for other options, or wonder “what’s the point?” and discontinue their benefits program altogether.

Limited opportunity for employees

The more perplexing the situation becomes for employers, the more employees feel the impact either in lower quality benefits, fewer options, more restrictions, or losing benefits altogether.

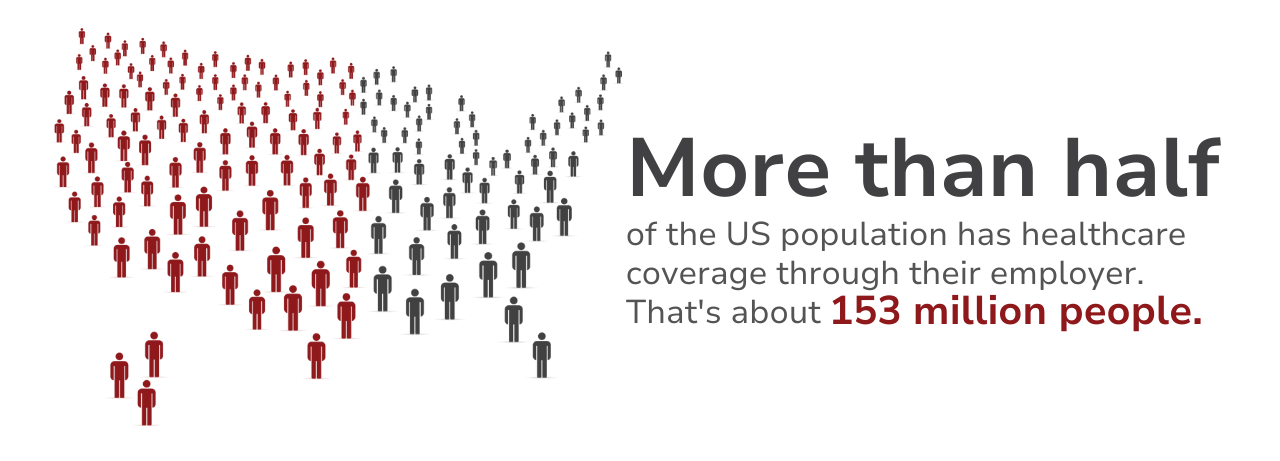

This is a critical situation since more than half of the US population gets their healthcare coverage from their employer (that’s about 153 million people).

Though this is the primary way that American’s access healthcare, only 53% of all companies in the US offer health benefits; and just half of small businesses offer health benefits. What this means is that many workers who might want health benefits through their employer, do not have the opportunity to do so. Furthermore, the more difficult it gets for all businesses, especially small and mid-size businesses to offer benefits, the less likely American workers are to have the option of employer-sponsored coverage. Many of these individuals are already looking for alternative options, while some are simply uninsured.

The more difficult it gets for businesses to offer benefits, the less likely American workers are to have the option of employer-sponsored coverage.

What can businesses do to face healthcare cost challenges?

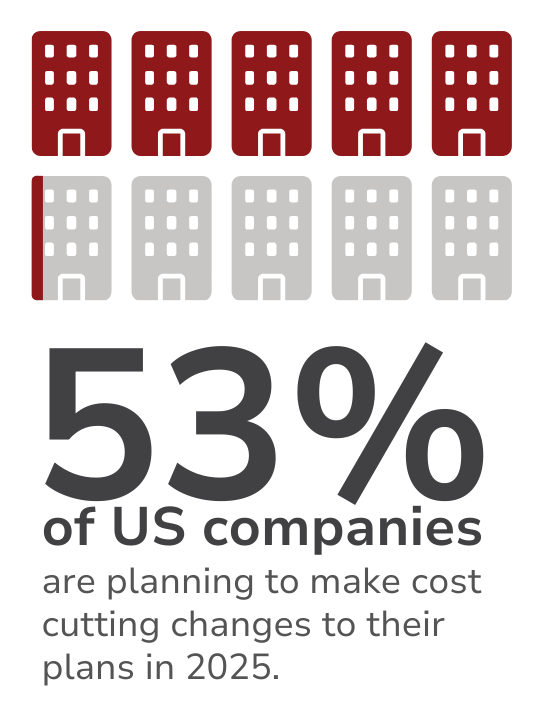

With looming premium price increases, 53% of companies are planning to make cost-cutting changes to their plans this coming year. What are your options if you are also trying to make sure your healthcare benefits are sustainable? Here’s what companies are trying, or are planning to try, in 2025.

Raise deductibles and adjusting cost sharing: This strategy keeps the healthcare coverage the same but reduces monthly premium expenses by having employees be responsible for more of their healthcare costs when they actually need to use it. By having employees share more of the cost when they have claims, you can reduce the overall plan costs.

Switch to cost-saving plan types like HMOs: With emphasis on care led by a primary care doctor, these plans save costs by having a medical professional guide care decisions, reducing specialist care, and working within a cost-saving network. Oftentimes, this helps you better predict and manage healthcare expenses for your team. On the other hand, the need for referrals on these plans can make them cumbersome for employees who have to use them.

Pick plans with very narrow networks: By partnering with very specific facilities or providers, plans may be able to negotiate even better prices while keeping their team with a familiar group of care providers. A plan like this will allow you to dramatically reduce the risk of overspending; however, employees may not care for the increased plan restrictions.

Find plans that use reference-based pricing: This strategy can really help manage healthcare costs because your plan will have fixed rates for paying claims. The plan will encourage employees to find providers who will work with plan rates to avoid paying the difference. While this type of approach can be effective, it may be too much of a burden on your team doing the homework to find appropriate providers.

Ditch the benefits program: As a last resort, you might consider dropping your benefits program—something companies have opted to do, allowing their employees to shop in the Marketplace for health coverage. Though this is a dramatic attempt at managing healthcare costs, your employees will see it as a pay cut, and you may need to compensate with some other health-oriented program, workplace perks, and higher wages (so they can afford those Marketplace plans).

Note: If you are a large employer and you are considering this route, you will want to carefully weigh the cost of the tax penalties you would be liable for. Some companies may find that paying the penalty, rather than “playing” by offering benefits may save them money, while others would end up paying more.

Shop for insurance alternatives:

As a compromise, you might start thinking about offering insurance alternatives for your employee benefits package. These can replace your traditional benefits package, or they can be mixed in with traditional options as a way for you to provide more options for your employees and still save money on healthcare costs.

What are some insurance alternatives for businesses?

Insurance alternatives may be new to you, and many of them are newer approaches to healthcare, though some have been around for a while. Generally, an insurance alternative is a solution that aims to help employees access healthcare outside of the traditional insurance model. Insurance alternatives provide valuable benefits while helping both employers and employees better manage healthcare expenses.

HDHP with HSA

A classic alternative that is closest to a traditional option is a high deductible health plan (HDHP) paired with a health savings account HSA. In this scenario, an employee can make tax-free contributions to their HSA and use those funds to pay for the healthcare they need until they meet their deductible. Since the health plan has a higher deductible, the monthly costs are lower. As a bonus, any unused funds roll over each year and can continue to grow tax-free.

There are various options for what kind of HDHP employers can choose to sponsor. A comprehensive health plan will provide more traditional coverage, while a preventive MEC plan will provided more limited benefits at a lower cost, allowing employers to contribute more to an employee’s HSA and still save money overall. Additionally, employers can decide to match HSA contributions up to a certain amount, or simply contribute a flat amount when employees choose this option.

DPC Membership

A direct primary care (DPC) membership focuses on access to routine care with a primary care provider that employees can build a quality relationship with. This is subscription-based healthcare where patients get unlimited access to their doctor for a flat monthly fee. The DPC doesn’t ever deal with insurance, allowing the provider to set the tone for their clinic, spend more time with patients, and focus on improved health outcomes rather than navigating insurance paperwork.

Employers can easily sponsor DPC memberships for their employees for predictable monthly fees. This option focuses on employees’ overall wellness, ensuring they have access to a doctor without any additional hurdles.

Medical Cost Sharing

Medical cost sharing has been around since the 1980s but is only recently becoming a viable insurance alternative for workplaces. Companies like Sedera Health and Zion HealthShare are making it possible for employers to offer medical cost sharing memberships as a benefit option for their employees. This option focuses on catastrophic care, the big scary medical bills that no one wants to ever deal with.

If you go down this route, you’ll pay a set monthly fee to sponsor the membership, you can split the cost with employees, or have them pay for it entirely. This kind of option can be paired with another alternative that focuses on everyday care for a more well-rounded healthcare solution. For example, pairing a HealthShare membership with a DPC membership has the potential to meet the needs of many employees while saving on overall costs.

Virtual Care

Virtual care goes by many names, telemedicine, telehealth, concierge medicine, and more. There are programs that focus on general medicine and provide a way for employees to call, text, or video chat with healthcare providers. More Americans than ever are using some form of telemedicine due to its convenience and cost effectiveness.

Employers can easily sponsor DPC memberships for their employees for predictable monthly fees....

...pairing a HealthShare membership with a DPC membership has the potential to meet the needs of many employees while saving on overall costs.

You can provide a general telemedicine program, or a more robust program like virtual primary care that will encompass concerns like mental health, weight counselling, and general patient advocacy.

Not every insurance alternative will be the right fit for every business’ employee population, but some alternatives, or a combination of insurance alternatives may give employers and employees the financial breathing room they need and more flexibility to decide how they want to spend their healthcare dollars.

What's next?

For the time being, healthcare costs continue to be a huge thorn in the side of businesses of all sizes. To escape the crushing weight of inflated costs and administrative tasks, employers are looking for insurance alternatives that will allow them to provide their employees with access to healthcare while protecting their bottom line. This ongoing challenge is spurring innovative approaches to healthcare cost management and promising efforts in healthcare technology.

In an upcoming article we will discuss in detail some of the insurance alternatives that are becoming more popular with employers, and how to talk to your employees about them.

End Notes:

*This is one way for large employers to calculate affordability (the rate is 8.39% for 2024 and 9.02% for 2025). Other methods are available such as the federal poverty line safe harbor. However, while other methods may be more straightforward, they may end up putting more financial responsibility on the employers.

**The IFEBP is predicting an average 8% increase, while Mercer is predicting between 5.8% and 7%.

Want to explore insurance alternatives for your business? Chat with one of our Benefit Guides about how insurance alternatives can add value to your benefits offering.

Explore

SUGGESTED FOR YOU